Call Prakash Acharya

Call Amrit Lamsal

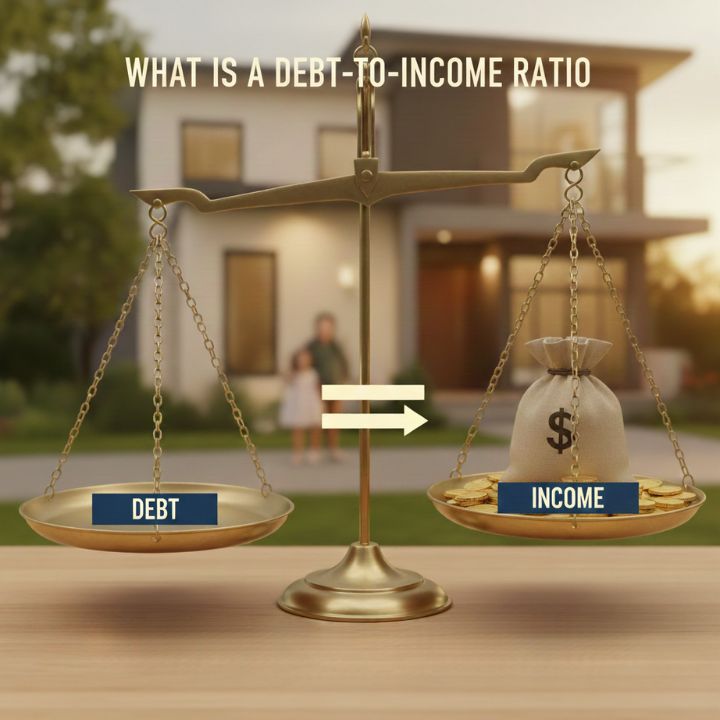

A debt-to-income ratio (DTI) is enough of a mouthful of a financial term that you would use when you take out a mortgage, but it does reveal a remarkably simple truth about your finances. Lenders rely on it to determine the extent to which you can comfortably accept new repayments without straining yourself thin. And as far as you are concerned, knowledge of your DTI may be the difference between being approved and getting a lower rate, or simply knowing that you have to sort a few things out before applying.

Having your DTI is an advantage (assuming you want to purchase a home, refinance your home loan, or even get a personal loan). Let’s break down what it is, how to calculate it, and why this simple debt ratio for home loans matters so much in Australia.

What Is a Debt-To-Income Ratio?

Your debt-to-income ratio is basically a snapshot of how much of your gross monthly income goes toward debt. Lenders love it because it gives them a fast, pretty realistic idea of your financial breathing room.

Debt-To-Income Ratio = Total Debt ÷ Gross Income

Definition:

It’s the percentage you get when you divide your total monthly debt repayments by your gross (before-tax) monthly income.

Why lenders care:

Banks are interested in determining whether you are comfortable handling a new loan in addition to what you already owe. A low DTI indicates that you are not overstretched. A high one makes them nervous, even if you feel fine day-to-day.

Quick example:

Assuming you earn a monthly income of $4,000 and that you owe a debt amounting to $1,000, your DTI is 25%. Pretty healthy.

How to Calculate Your Debt-To-Income Ratio

The good news: calculating your DTI is easier than trying to understand half the jargon on your home loan contract.

Here’s the step-by-step:

- Add up your monthly debt payments.

Think about minimum credit card repayments, personal loans, car loans, student loans, buy-now-pay-later commitments, and the estimated mortgage repayment if you’re applying for a home loan. - Divide that number by your gross monthly income.

That’s your income before tax or super contributions. - Multiply by 100.

That gives you your DTI percentage.

Example:

- Gross Monthly Income: $5,000

- Monthly Debts: $1,500

- DTI = ($1,500 ÷ $5,000) × 100 = 30%

If maths isn’t your thing, an online debt-to-income ratio calculator will do the heavy lifting in seconds.

Ideal Debt-To-Income Ratios for Borrowers

Every bank has its own internal rules, but most Australian lenders tend to follow similar benchmarks:

| DTI Range | Financial Position | Lending Risk |

| Less than 36% | Strong | Low (favoured by lenders) |

| 36%– 43% | Acceptable | Moderate (still workable) |

| Above 43% | Risky | High (likely to be declined) |

For first home buyer loans in Australia, staying under about 40% gives you the best chance of approval and better interest rate options. When rates move, lenders want to know you have enough buffer to keep making repayments without stress.

Why Debt-To-Income Ratio Matters for Home Loans

Your DTI can influence your home loan outcome more than you might expect. Lenders use it as a quick snapshot of your financial health-how much you earn versus how much you owe- and it often becomes a deciding factor long before they look at the finer details of your application.

It affects:

- Your risk profile: A higher DTI signals to lenders that a larger share of your income is tied up in existing commitments, which increases your perceived risk.

- Your interest rate: The lower the DTI of the applicants, the more financially stable they are, and they have a better bargaining power to obtain more competitive rates.

- Your approval chances: Banks can delay the process, demand supporting documents, or even require you to reduce or close some of your debts before they proceed with granting you approval.

A surprisingly large number of borrowers get knocked back simply because they didn’t check this number first. Understanding your DTI early gives you time to improve it-and puts you in a much stronger position when it’s time to apply.

How to Improve Your Debt-To-Income Ratio

If your DTI looks a bit too high, don’t panic; there are practical ways to bring it down.

- Tackle high-interest debt first. Credit card balances and personal loans significantly impact the DTI.

- Avoid taking new loans for a while. Even a small car loan can tip your ratio.

- Increase your income (if possible). A salary bump, side income, or promotion can instantly change your DTI.

- Consider debt consolidation. Combining debts into one loan with a lower interest rate can reduce your total monthly repayments-just make sure the longer term doesn’t cost you more overall.

Even shaving a few hundred dollars off your monthly obligations can make your DTI dramatically more lender-friendly.

Debt-To-Income Ratio vs Other Financial Metrics

Lenders don’t look at DTI alone. It’s just one piece of a broader financial profile they build to understand how safely you can manage a home loan. When they assess your borrowing capacity, they combine several indicators to get a more accurate picture of your long-term financial behaviour- not just your monthly numbers.

Here’s what else they consider:

Loan-to-Value Ratio (LVR):

This compares the amount you want to borrow with the property’s market value. A high LVR (meaning you’re borrowing most of the property price) signals higher risk because you have less equity. Borrowers with lower LVRs are typically rewarded with better interest rates and fewer lending conditions.

Credit Score:

Your credit score reflects how reliably you’ve managed debt in the past-credit cards, personal loans, buy-now-pay-later accounts, and more. A strong credit score can soften concerns around a slightly higher DTI, while a poor score may amplify them. Banks want to see evidence of consistent repayments and responsible lending behaviour.

Savings Behaviour:

While not a formal metric, your saving habits matter. Lenders check whether you have a history of genuine savings, because it suggests discipline and financial stability. Regular contributions to a savings account-even small ones-can boost your overall profile and balance out other weaknesses.

Loan-to-Income Ratio (LTI):

- Australia also uses LTI, particularly for larger loan amounts or high-income applicants.

- DTI shows short-term affordability- how easily you can manage repayments month to month.

- LTI looks at the size of your total debt compared to your annual income indicator of how stretched you might become over time.

Together, these metrics help lenders assess both your immediate repayment capacity and your long-term financial resilience. A strong overall profile can compensate for a slightly higher DTI, but a weak combination can limit how much a bank is willing to lend-even if your DTI looks acceptable on paper.

Common Questions About Debt-To-Income Ratio

Q1: What is a good debt-to-income ratio for getting a home loan?

A good DTI depends on how the lender measures it. In Australia, most lenders look at both your monthly DTI and your total debt vs annual income:

Monthly DTI:

- Below 36% = strong

- 36%–43% = acceptable

- Above 43% = high risk

DTI based on annual income (commonly used by Australian lenders):

- 3–5 = good

- 6+ = considered risky

- 7–8+ = may trigger stricter checks or declines

Overall, a lower DTI improves your approval chances and helps you secure better loan terms, but lenders still consider other factors like LVR, income stability, savings history, and credit score.

Q2: Can I apply for a loan if my DTI is high?

You can try, but approval becomes tougher. A large deposit or strong financial history might still get you across the line.

Q3: How does DTI affect interest rates?

Lower DTI usually leads to stronger offers and more competitive rates. Higher DTI often means fewer options.

Q4: Can I use a debt-to-income ratio calculator online?

Yes, banks and comparison websites offer free calculators that are easy to use.

Q5: What’s the difference between DTI and the loan-to-income ratio in Australia?

Debt-to-Income Ratio (DTI) compares your monthly debt repayments to your monthly income. It shows how comfortably you can manage ongoing repayments.

Loan-to-Income Ratio (LTI) compares your total loan amount to your annual income. It shows whether the overall size of the loan is reasonable based on what you earn.

In simple terms:

- DTI = monthly affordability

- LTI = total borrowing size

Australian lenders often use both to assess risk.

Q6: How often should I check my DTI?

Any time you’re planning a major financial decision, especially before applying for a home loan.

Q7: Can consolidating debts help improve DTI?

Yes, if it lowers your total monthly repayment. Just be careful with longer terms that increase the total interest paid.

Contact Capkon today for more detailed info about the debt-to-income ratio. Our team of professional mortgage experts are only one call away for all your queries!

A mortgage application is a large financial commitment that you will encounter. It is not only about having a house in your pocket- it is about establishing long-term financial stability.

Although acquiring the right home loan will save you thousands in the long run, a little slip in the process may cause delay, refusal, or unwarranted expenses. Whether it is a first-time buyer home loan or refinancing, it is better to know what not to do, which can be the difference.

This guide discusses the most common pitfalls one should avoid before applying for a mortgage and how to prevent them.

Common Mortgage Mistakes to Avoid

It is important to know the pitfalls that may undermine your application or add to its cost before nailing down a home loan. Most of them are mere negligence that might lead to long-term effects in case they are not detected early.

Applying Without Checking Your Credit Score

Your credit score is a key part of every mortgage application. It shows lenders how well you manage your financial obligations. Scheduling an appointment without looking at it is a way to be caught off guard – by old defaults, delayed payments, or false listings that may negatively affect your application.

What to do: Get a free copy of your credit report from major Australian credit reporting agencies like Equifax or Experian. Before applying, ensure you are paying down the debts where appropriate, check on mistakes, and ensure that the scores of your financial behaviour are accurately reflected.

Taking on New Debt Before Applying

Avoid opening new credit cards, taking out car loans, or using buy-now-pay-later services before applying for a mortgage. These debts reduce your borrowing capacity and may make lenders view you as a higher risk.

Lenders assess your total financial commitments, so even if you can afford repayments now, new obligations can affect how much you’re allowed to borrow.

Ignoring Hidden Fees

A low interest rate might look attractive, but fees can quickly erode potential savings. Application fees, monthly account fees, and Lenders Mortgage Insurance (LMI) are just a few examples of costs that many borrowers overlook.

Tip: Always ask for a loan’s comparison rate, which includes interest and standard fees, giving you a clearer view of the true cost.

Failing to Compare Lenders and Loan Products

Many borrowers simply go to their main bank, assuming it’s the best option. In reality, different lenders offer a range of rates, policies, and features. Some are better suited to first-home buyers; others cater to investors or self-employed applicants.

Comparing multiple lenders and loan types ensures you’re not missing out on a deal that fits your situation better. Even a 0.25% difference in interest rate can save thousands over the life of a mortgage.

Overestimating Your Borrowing Capacity

Simply because you are entitled to a given amount does not imply that you should take it. The debt to the hilt may have you susceptible to financial strain in case interest rates go up or your financial condition alters.

Calculate the amount of the repayment that fits in your monthly finances and leaves you with space to handle other expenses and future aspirations.

Overlooking Your Long-Term Financial Goals

A lot of buyers are preoccupied with getting approved and never meditate on how the mortgage will fit into their larger financial picture.

Mortgage is not a matter of having a house but a way of living and a decades-long establishing financial stability.

Assess Future Income and Career Changes

Consider the way your income will change. Do you plan a study break, parental leave or a change of career? Will your income level rise or fall drastically? Select a loan model that will allow flexibility in such possibilities.

Plan for Life Events

Major milestones like marriage, children, or starting a business can all affect your ability to make repayments. Planning for these events ensures you won’t have to make rushed financial decisions later.

Think About Exit Strategies

Consider how easy it is to refinance, sell, or pay off your loan early. Some fixed-rate loans come with break fees if you exit early, while others offer flexible features that make refinancing smoother.

Avoid Overextending

When a lender provides more than you are anticipating, it may be tempting to accept it. However, it may be something that your future self will regret. Borrow an amount that you can comfortably repay to have room to save, have an emergency fund and adjust your lifestyle accordingly.

Example: A couple that takes a loan to the fullest value without considering future childcare costs might easily experience severe financial stress in a few years.

Failing to Review Your Employment and Income Documentation

One of the main reasons mortgage applications get delayed or rejected is incomplete or inconsistent documentation. Australian lenders are strict about verifying income to ensure borrowers can handle repayments.

Gather the Right Documents

Before you apply, collect the following:

- Recent payslips showing your income and employer details

- At least two years of tax returns and assessment notices

- Employment letters verifying your role and income

- Bank statements showing regular salary deposits

For self-employed applicants, add:

- Business financial statements for the last two years

- BAS statements

- A letter from your accountant verifying your income

Check for Consistency

Make sure all figures across documents, including payslips, tax returns, and your application, line up. Even small discrepancies can lead to delays as lenders ask for clarification.

Example: A buyer with a casual contract, assuming it counts as full-time income, may have their application rejected because the lender can’t verify consistent earnings.

Not Understanding Your Loan Options

There are many types of home loans, and each one affects how you manage repayments and interest over time. Choosing the wrong structure can be an expensive mistake.

Fixed, Variable, or Split Loans

- Fixed-rate loans lock in your interest rate for a period (usually 1–5 years), offering repayment certainty. However, they often come with restrictions on extra repayments and refinancing.

- Variable-rate loans move with market interest rates, meaning your repayments can go up or down. They’re usually more flexible but come with uncertainty.

- Split-rate loans combine both a fixed part variable offering a balance of stability and flexibility.

Loan Features Matter

Offset accounts, redraw facilities, and the ability to make extra repayments can save you years off your loan term and reduce interest paid.

Choosing the Right Option

Consider how long you plan to stay in your property, your comfort with rate changes, and your long-term goals before deciding.

Skipping Pre-Approval

Pre-approval gives you a clear picture of how much you can borrow before you start house hunting. It’s not a full loan approval, but it’s a strong indication from a lender that you’re eligible within certain limits.

Benefits of Pre-Approval

- Helps you set a realistic budget

- Strengthens your negotiating power with agents and sellers

- Speeds up the formal approval process once you’ve found a property

Risks of Skipping It

Without pre-approval, you risk falling in love with a home you can’t afford or missing out on one because your finances aren’t ready.

Example: A buyer who skips pre-approval might make an offer on a property only to discover later that the lender won’t approve the full loan amount.

Not Budgeting for Additional Costs

Buying a home involves far more than just the deposit. Many applicants underestimate the full cost of purchasing and maintaining a property.

Upfront Costs

- Deposit (typically 5–20% of the purchase price)

- Stamp duty (varies by state)

- Loan application and valuation fees

- Legal and conveyancing costs

- Building and pest inspections

Ongoing Costs

- Home and contents insurance

- Council rates and water charges

- Strata fees (if applicable)

- Repairs and maintenance

Failing to budget for these can leave you short of cash when you need it most- or worse, unable to complete your purchase.

Ignoring Your Debt-to-Income Ratio

Your debt-to-income ratio (DTI) measures how much of your income is already committed to paying off existing debts. It’s a major factor lenders use to assess your ability to handle a mortgage.

A high DTI can reduce your borrowing capacity or result in a declined application.

How to Improve It

- Pay off or reduce credit card balances

- Consolidate personal loans where possible

- Avoid taking on any new debt before applying

- Lower your credit limits to reduce your perceived risk

Monitoring and improving your DTI before you apply makes your application stronger and shows lenders you’re financially disciplined.

Relying Only on Interest Rates

A low interest rate might look appealing, but it doesn’t always mean the cheapest loan. Some low-rate products come with high ongoing fees, limited flexibility, or expensive penalties for early repayments.

What Else to Consider

- Comparison rates (which include most standard fees)

- Flexibility for extra repayments

- Access to redraw or offset accounts

- Break fees on fixed-rate loans

Example: A loan with a slightly higher rate but an offset account can save more interest over time than a low-rate loan with no flexible features.

Not Seeking Professional Advice

Navigating the mortgage process can be complex and mistakes can be expensive. Working with a qualified mortgage broker or financial adviser can help you understand your options and avoid pitfalls.

Why Expert Advice Helps

- Brokers can compare products across multiple lenders

- They understand lending criteria and policy differences

- They can identify which loans suit your goals and situation

- They handle much of the paperwork, saving time and stress

When choosing a broker, ensure they’re accredited, transparent about fees, and have experience with your type of property or buyer profile.

Steps to Avoid Mortgage Mistakes

To set yourself up for success, take these practical steps guaranteed to approve a loan before applying:

- Check your credit report and correct any errors.

- Calculate your debt-to-income ratio and improve it where possible.

- Research lenders and loan types to find one that fits your goals.

- Budget carefully for both upfront and ongoing costs.

- Get expert advice before submitting your application.

Taking the time to prepare can mean faster approval, lower stress, and a home loan that works for your future.

Ready to Avoid Mortgage Mistakes? Speak With an Expert Today!

Purchasing a house is fun, yet it is a big financial move. By eliminating these pitfalls, you will go into the process of applying for a mortgage with clarity and confidence.

Unless you really know what you want, a qualified mortgage broker or best financial advisor in Melbourne can help you compare and contrast options, prepare your paperwork and walk you through the entire process.

Contact CapKon and have a detailed consultation with our experts today! Better now than never to avoid any mistakes before applying for your mortgage.

FAQs

Q1: What are the biggest mistakes first-time homebuyers make?

Overborrowing, skipping pre-approval, ignoring extra costs, and failing to compare lenders are some of the most common errors.

Q2: How can I check if I’m ready for a mortgage?

Review your savings, income stability, and existing debts. If you can comfortably afford repayments plus living costs, you’re likely in a good position.

Q3: Should I get pre-approval before house hunting?

Yes. It clarifies your budget, strengthens your offers, and speeds up final approval when you find the right property.

Q4: How does my credit score affect my mortgage application?

A higher score can mean better rates and smoother approval. Lenders see it as a sign of responsible borrowing.

Q5: What hidden costs should I budget for before applying?

Include stamp duty, legal fees, inspections, and insurance alongside your deposit.

Q6: Can a mortgage broker help me avoid mistakes?

Absolutely. Brokers can identify the right lender, structure your application correctly, and save you time and stress.

Buying your first home in Australia has always been a challenge with high deposits, rising property prices, and strict eligibility rules. But from 1 October 2025, the government is making major changes to the First Home Guarantee (FHG), making it easier for first-time buyers to get into the market sooner.

At Capkon Melbourne, we specialise in helping first-home buyers refinance, navigate schemes like this, and secure the right home loan in Asutralia. Here’s a full breakdown of what’s changing and how you could benefit.

What Is the First Home Guarantee?

The First Home Guarantee is a government project that aims to enable Australian citizens to buy a house with a smaller deposit. Conventionally, the deposit that lenders demand is 20% of the value of the home being purchased. With a loan amount lower than 20%, you would normally be expected to pay Lenders Mortgage Insurance (LMI).

The FHG acts as a government guarantee for a portion of your home loan, typically up to 15%. This allows you to get a home loan at a low deposit of as little as 5% and you also save many tens of thousands of dollars in the big cost of LMI. It has also turned a lot of lives around since those who would not have been able to save the entire 20% deposit would have done that.

What’s Changing from 1 October 2025?

The October 2025 update introduces the biggest expansion to date, making the scheme more accessible to a wider range of first-home buyers. The key changes include:

- Unlimited places: The previous annual cap on the number of available spots is being removed. This means all eligible first home buyers can apply, eliminating the need to rush for a limited spot.

- No income limits: The existing income caps (previously $125,000 for individuals and $200,000 for couples) are being scrapped. This opens the scheme to more buyers, including those with higher incomes who still face challenges saving a large deposit.

- Higher property price caps: The price limits for eligible properties are being raised significantly to reflect current market values. This gives buyers more options and flexibility in where they can purchase a home.

- Simplified regional access: The separate Regional First Home Buyer Guarantee will be integrated into the First Home Guarantee, streamlining the process for those buying outside major capital cities.

New Property Price Caps Across Australia

The higher property price caps are a major part of the new changes. They are being adjusted to better align with the median house prices in each state and territory. Here are the new maximum property values under the FHG (effective 1 October 2025):

| Capital City | New Cap (Oct 2025) |

| Sydney (NSW) | $1.5M |

| Melbourne (VIC) | $950K |

| Brisbane (QLD) | $1M |

| Perth (WA) | $850K |

| Adelaide (SA) | $900K |

| Canberra (ACT) | $1M |

| Darwin (NT) | $600K |

| Hobart (TAS) | $700K |

Regional areas also have higher limits, meaning more choice and flexibility for first-home buyers.

Example – Buying with a 5% Deposit in 2025

Let’s look at a real-world example of how the new rules can help a first-home buyer in Melbourne.

With the new FHG criteria, they require a deposit of a mere 5% amounting to only $30,000. The government will guarantee that they will be able to borrow 95% of the property value as a home loan, and will not pay Lenders Mortgage Insurance (LMI,) which saves them thousands of dollars.

Avoiding LMI with the First Home Guarantee

Lenders Mortgage Insurance (LMI) is a single payment that provides the lender with protection, and not the borrower, in the event that you default on the mortgage. Banks usually need it when borrowing less than 20% of the total deposit because it is their method of containing risk. The cost of LMI can be significant, often adding tens of thousands of dollars to your upfront costs.

The FHG allows you to bypass LMI completely. For example, on a home in Melbourne valued at the new $950,000 price cap, the LMI could be well over $20,000. The FHG allows you to avoid this cost entirely, making a substantial difference to your total savings and upfront costs.

Who Is Eligible for the 2025 FHG?

With the updated rules, the FHG is now open to more buyers. To be eligible, you must meet the following criteria:

- Citizenship: Be an Australian citizen or a permanent resident.

- First Home Buyer: You must be a first home buyer, meaning you have never owned a property in Australia before.

- Property Type: The property must be for residential use and you must intend to be an owner-occupier. It can be an existing home, a new build, or a house and land package.

- Deposit: You must have a minimum deposit of 5% of the property value.

- Property Price: The property’s value must be at or below the new price caps for your location.

Breaking Down the Costs Beyond the Deposit

While the FHG significantly reduces your deposit requirement and helps you avoid LMI, it’s crucial to remember there are other costs to budget for. These upfront costs include:

- Stamp duty: This is a state government tax on property purchases. In Victoria, first home buyers may be eligible for a stamp duty concession or exemption depending on the property’s value.

- Legal & conveyancing fees: These cover the legal costs of transferring ownership of the property.

- Inspections: Pre-purchase building and pest inspections.

- Bank & application fees: Various fees charged by your lender.

In the case of a property in Melbourne valued at $700 000 a deposit of 5% will be 35,000. Although you would save on LMI, you would still have to have extra cash to cover expenses such as stamp duty (where you can be provided with a concession), legal fees and other miscellaneous expenses.

Alternative Support Options for First Home Buyers

The FHG is not the only option available. Capkon Melbourne can also help you explore other pathways to home ownership, such as:

- Victorian Homebuyer Fund (Shared Equity): The Victorian government co-purchases a percentage of your home (up to 25%), which reduces the amount you need to borrow.

- Guarantor Loans: A family member, typically a parent, uses the equity in their own home as security for your loan. This can help you avoid LMI and may even allow you to borrow up to 100% of the property’s value.

Why Work with Capkon Melbourne for Your First Home Loan?

Navigating the FHG and other government schemes can be complex. At Capkon Melbourne, we are more than just mortgage brokers in Melbourne; we are your dedicated partners in your home-buying journey.

- Specialised Expertise: We specialise in first-home buyer loans and have in-depth knowledge of all government schemes.

- Streamlined Process: We handle the eligibility checks, paperwork, and applications for you, ensuring a smooth and stress-free process.

- Access to Multiple Lenders: We work with a wide panel of lenders, giving you access to the best rates and loan products.

- Personalised Guidance: We provide step-by-step guidance, from your initial consultation to settlement, answering all your questions along the way.

Should You Enter the Market Now?

The changes to the First Home Guarantee from October 2025 are a game-changer. With unlimited places and higher property price caps, the scheme will become more accessible than ever, and the competition for spots will disappear. This gives you more time and choice to find the right property.

Now is the perfect time to plan ahead and get your finances in order. Contact Capkon Melbourne today to start your first home journey and take the first step towards securing your dream home.

FAQ related to Changes Coming to the First Home Guarantee (FHG) in 2025

What is the First Home Guarantee?

The First Home Guarantee is a government scheme that helps eligible first home buyers purchase a home with a 5% deposit and avoid paying Lenders Mortgage Insurance (LMI).

How much deposit do I need in 2025 to buy a home?

Under the First Home Guarantee, you can buy a home with a minimum of a 5% deposit.

Can I buy in Melbourne with just a 5% deposit?

Yes, with the First Home Guarantee, eligible buyers can purchase a property in Melbourne with a deposit of 5% and no LMI.

Do I still need to pay LMI under the FHG?

No, the key benefit of the FHG is that the government guarantees a portion of your loan, so you do not have to pay LMI.

What are the new property price caps in 2025?

The new price caps, effective 1 October 2025, are $1.5M in Sydney, $950K in Melbourne, and $900K in Adelaide, among others.

Can couples apply together?

Yes, the scheme is available for individuals and joint applicants, including couples.

What if I’ve owned property before?

To be eligible for the FHG, you must be a first-home buyer and have never owned property in Australia before.

How does the FHG differ from Shared Equity schemes?

The FHG is a government guarantee that helps you secure a low-deposit loan and avoid LMI. Shared equity schemes, like the Victorian Homebuyer Fund, involve the government co-purchasing a portion of your home.

Is there still a limit on the number of places?

From 1 October 2025, the annual cap on places for the First Home Guarantee will be removed.

Can I use my super for a home deposit?

The First Home Super Saver Scheme (FHSSS) allows eligible first home buyers to make voluntary contributions to their superannuation and withdraw them to use as a deposit.

Do you need any Assistance in your loan?

We are here to help you.