Call Prakash Acharya

Call Amrit Lamsal

A mortgage application is a large financial commitment that you will encounter. It is not only about having a house in your pocket- it is about establishing long-term financial stability.

Although acquiring the right home loan will save you thousands in the long run, a little slip in the process may cause delay, refusal, or unwarranted expenses. Whether it is a first-time buyer home loan or refinancing, it is better to know what not to do, which can be the difference.

This guide discusses the most common pitfalls one should avoid before applying for a mortgage and how to prevent them.

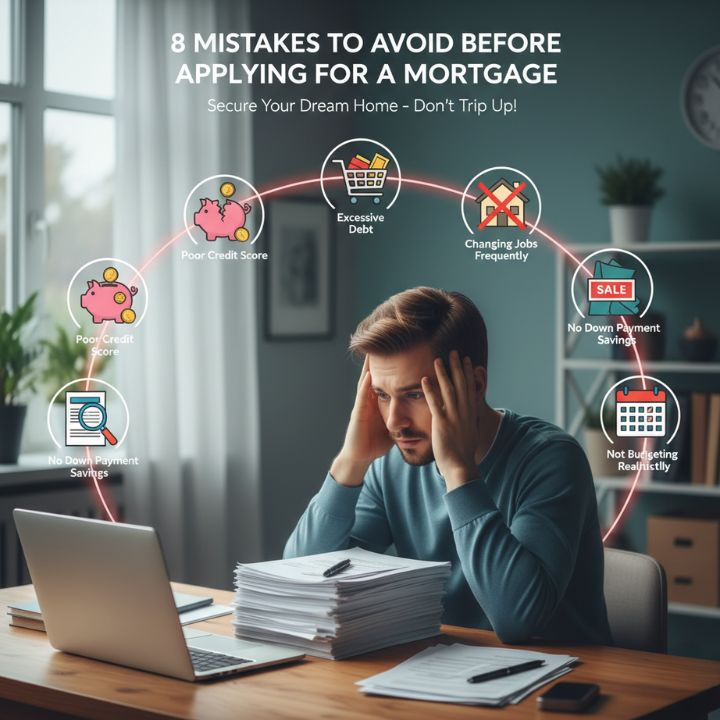

Common Mortgage Mistakes to Avoid

It is important to know the pitfalls that may undermine your application or add to its cost before nailing down a home loan. Most of them are mere negligence that might lead to long-term effects in case they are not detected early.

Applying Without Checking Your Credit Score

Your credit score is a key part of every mortgage application. It shows lenders how well you manage your financial obligations. Scheduling an appointment without looking at it is a way to be caught off guard – by old defaults, delayed payments, or false listings that may negatively affect your application.

What to do: Get a free copy of your credit report from major Australian credit reporting agencies like Equifax or Experian. Before applying, ensure you are paying down the debts where appropriate, check on mistakes, and ensure that the scores of your financial behaviour are accurately reflected.

Taking on New Debt Before Applying

Avoid opening new credit cards, taking out car loans, or using buy-now-pay-later services before applying for a mortgage. These debts reduce your borrowing capacity and may make lenders view you as a higher risk.

Lenders assess your total financial commitments, so even if you can afford repayments now, new obligations can affect how much you’re allowed to borrow.

Ignoring Hidden Fees

A low interest rate might look attractive, but fees can quickly erode potential savings. Application fees, monthly account fees, and Lenders Mortgage Insurance (LMI) are just a few examples of costs that many borrowers overlook.

Tip: Always ask for a loan’s comparison rate, which includes interest and standard fees, giving you a clearer view of the true cost.

Failing to Compare Lenders and Loan Products

Many borrowers simply go to their main bank, assuming it’s the best option. In reality, different lenders offer a range of rates, policies, and features. Some are better suited to first-home buyers; others cater to investors or self-employed applicants.

Comparing multiple lenders and loan types ensures you’re not missing out on a deal that fits your situation better. Even a 0.25% difference in interest rate can save thousands over the life of a mortgage.

Overestimating Your Borrowing Capacity

Simply because you are entitled to a given amount does not imply that you should take it. The debt to the hilt may have you susceptible to financial strain in case interest rates go up or your financial condition alters.

Calculate the amount of the repayment that fits in your monthly finances and leaves you with space to handle other expenses and future aspirations.

Overlooking Your Long-Term Financial Goals

A lot of buyers are preoccupied with getting approved and never meditate on how the mortgage will fit into their larger financial picture.

Mortgage is not a matter of having a house but a way of living and a decades-long establishing financial stability.

Assess Future Income and Career Changes

Consider the way your income will change. Do you plan a study break, parental leave or a change of career? Will your income level rise or fall drastically? Select a loan model that will allow flexibility in such possibilities.

Plan for Life Events

Major milestones like marriage, children, or starting a business can all affect your ability to make repayments. Planning for these events ensures you won’t have to make rushed financial decisions later.

Think About Exit Strategies

Consider how easy it is to refinance, sell, or pay off your loan early. Some fixed-rate loans come with break fees if you exit early, while others offer flexible features that make refinancing smoother.

Avoid Overextending

When a lender provides more than you are anticipating, it may be tempting to accept it. However, it may be something that your future self will regret. Borrow an amount that you can comfortably repay to have room to save, have an emergency fund and adjust your lifestyle accordingly.

Example: A couple that takes a loan to the fullest value without considering future childcare costs might easily experience severe financial stress in a few years.

Failing to Review Your Employment and Income Documentation

One of the main reasons mortgage applications get delayed or rejected is incomplete or inconsistent documentation. Australian lenders are strict about verifying income to ensure borrowers can handle repayments.

Gather the Right Documents

Before you apply, collect the following:

- Recent payslips showing your income and employer details

- At least two years of tax returns and assessment notices

- Employment letters verifying your role and income

- Bank statements showing regular salary deposits

For self-employed applicants, add:

- Business financial statements for the last two years

- BAS statements

- A letter from your accountant verifying your income

Check for Consistency

Make sure all figures across documents, including payslips, tax returns, and your application, line up. Even small discrepancies can lead to delays as lenders ask for clarification.

Example: A buyer with a casual contract, assuming it counts as full-time income, may have their application rejected because the lender can’t verify consistent earnings.

Not Understanding Your Loan Options

There are many types of home loans, and each one affects how you manage repayments and interest over time. Choosing the wrong structure can be an expensive mistake.

Fixed, Variable, or Split Loans

- Fixed-rate loans lock in your interest rate for a period (usually 1–5 years), offering repayment certainty. However, they often come with restrictions on extra repayments and refinancing.

- Variable-rate loans move with market interest rates, meaning your repayments can go up or down. They’re usually more flexible but come with uncertainty.

- Split-rate loans combine both a fixed part variable offering a balance of stability and flexibility.

Loan Features Matter

Offset accounts, redraw facilities, and the ability to make extra repayments can save you years off your loan term and reduce interest paid.

Choosing the Right Option

Consider how long you plan to stay in your property, your comfort with rate changes, and your long-term goals before deciding.

Skipping Pre-Approval

Pre-approval gives you a clear picture of how much you can borrow before you start house hunting. It’s not a full loan approval, but it’s a strong indication from a lender that you’re eligible within certain limits.

Benefits of Pre-Approval

- Helps you set a realistic budget

- Strengthens your negotiating power with agents and sellers

- Speeds up the formal approval process once you’ve found a property

Risks of Skipping It

Without pre-approval, you risk falling in love with a home you can’t afford or missing out on one because your finances aren’t ready.

Example: A buyer who skips pre-approval might make an offer on a property only to discover later that the lender won’t approve the full loan amount.

Not Budgeting for Additional Costs

Buying a home involves far more than just the deposit. Many applicants underestimate the full cost of purchasing and maintaining a property.

Upfront Costs

- Deposit (typically 5–20% of the purchase price)

- Stamp duty (varies by state)

- Loan application and valuation fees

- Legal and conveyancing costs

- Building and pest inspections

Ongoing Costs

- Home and contents insurance

- Council rates and water charges

- Strata fees (if applicable)

- Repairs and maintenance

Failing to budget for these can leave you short of cash when you need it most- or worse, unable to complete your purchase.

Ignoring Your Debt-to-Income Ratio

Your debt-to-income ratio (DTI) measures how much of your income is already committed to paying off existing debts. It’s a major factor lenders use to assess your ability to handle a mortgage.

A high DTI can reduce your borrowing capacity or result in a declined application.

How to Improve It

- Pay off or reduce credit card balances

- Consolidate personal loans where possible

- Avoid taking on any new debt before applying

- Lower your credit limits to reduce your perceived risk

Monitoring and improving your DTI before you apply makes your application stronger and shows lenders you’re financially disciplined.

Relying Only on Interest Rates

A low interest rate might look appealing, but it doesn’t always mean the cheapest loan. Some low-rate products come with high ongoing fees, limited flexibility, or expensive penalties for early repayments.

What Else to Consider

- Comparison rates (which include most standard fees)

- Flexibility for extra repayments

- Access to redraw or offset accounts

- Break fees on fixed-rate loans

Example: A loan with a slightly higher rate but an offset account can save more interest over time than a low-rate loan with no flexible features.

Not Seeking Professional Advice

Navigating the mortgage process can be complex and mistakes can be expensive. Working with a qualified mortgage broker or financial adviser can help you understand your options and avoid pitfalls.

Why Expert Advice Helps

- Brokers can compare products across multiple lenders

- They understand lending criteria and policy differences

- They can identify which loans suit your goals and situation

- They handle much of the paperwork, saving time and stress

When choosing a broker, ensure they’re accredited, transparent about fees, and have experience with your type of property or buyer profile.

Steps to Avoid Mortgage Mistakes

To set yourself up for success, take these practical steps guaranteed to approve a loan before applying:

- Check your credit report and correct any errors.

- Calculate your debt-to-income ratio and improve it where possible.

- Research lenders and loan types to find one that fits your goals.

- Budget carefully for both upfront and ongoing costs.

- Get expert advice before submitting your application.

Taking the time to prepare can mean faster approval, lower stress, and a home loan that works for your future.

Ready to Avoid Mortgage Mistakes? Speak With an Expert Today!

Purchasing a house is fun, yet it is a big financial move. By eliminating these pitfalls, you will go into the process of applying for a mortgage with clarity and confidence.

Unless you really know what you want, a qualified mortgage broker or best financial advisor in Melbourne can help you compare and contrast options, prepare your paperwork and walk you through the entire process.

Contact CapKon and have a detailed consultation with our experts today! Better now than never to avoid any mistakes before applying for your mortgage.

FAQs

Q1: What are the biggest mistakes first-time homebuyers make?

Overborrowing, skipping pre-approval, ignoring extra costs, and failing to compare lenders are some of the most common errors.

Q2: How can I check if I’m ready for a mortgage?

Review your savings, income stability, and existing debts. If you can comfortably afford repayments plus living costs, you’re likely in a good position.

Q3: Should I get pre-approval before house hunting?

Yes. It clarifies your budget, strengthens your offers, and speeds up final approval when you find the right property.

Q4: How does my credit score affect my mortgage application?

A higher score can mean better rates and smoother approval. Lenders see it as a sign of responsible borrowing.

Q5: What hidden costs should I budget for before applying?

Include stamp duty, legal fees, inspections, and insurance alongside your deposit.

Q6: Can a mortgage broker help me avoid mistakes?

Absolutely. Brokers can identify the right lender, structure your application correctly, and save you time and stress.

The process of being approved to take a mortgage loan may be daunting, particularly when you are purchasing a house, and this is your first time. Every step matters, as far as knowing what lenders need to your finances. At Capkon Melbourne, we help borrowers navigate the process and understand what lenders want, as well as what borrowers can do to improve their chances of approval. This guide will cover the steps to take when applying for a mortgage loan, the key considerations lenders take into account, and offer professional tips to help you ensure you are approved.

What Mortgage Approval Means

Mortgage approval is merely a lender verifying your funds and property value and then formally deciding to lend you a certain amount of money on certain terms and conditions.

It’s helpful to know the difference between pre-approval and full approval:

- Pre-Approval: It is a preliminary test in which a lender analyses your income, assets and debts. Then they provide you with an approximation of the amount that they are willing to lend. This will be an important step since you will have a realistic budget to start house hunting.

- Full Approval (Conditional or Unconditional): It is the last commitment. It normally involves an official assessment of the property you intend to purchase and a final review of all your papers. Unconditional approval is an approval that the lender has granted a final go-ahead, and the loan is good to be settled.

Why does one need to seek approval before he or she go house hunting? Pre-approval will also ensure that you are confident in your budget, sellers know that you are a serious buyer, and it can also enable you to make fast decisions once you have located the right property. This renders the process of being approved to borrow a mortgage loan the most significant point of commencement of a home-buying adventure.

How to Apply for a Mortgage Loan

The process of how to apply for a mortgage loan requires preparation and close attention to detail. Follow these steps for a smoother application:

- Check Your Credit Score and Financial Health: Get a copy of your credit report to check for errors and see your current score. Pay off any small, outstanding debts if you can.

- Gather Documents: Lenders need a lot of documentation. This typically includes:

- Proof of Income: Recent payslips, employment letters, or tax returns (if you’re self-employed).

- Bank Statements: Showing your savings history and current balances.

- Identification: Driver’s license, passport.

- Debt Statements: Credit card statements and existing loan balances.

- Compare Lenders and Home Loan Products: Don’t just stick with your current bank. Research different options like banks, credit unions, and non-bank lenders and compare interest rates, fees, and loan features. This is where getting professional help can save you money.

- Submit Application and Pre-Approval Request: Once you decide on a lender or broker, you will complete a formal application, often including a request for pre-approval.

- Respond to Lender Queries: The lender will review your application and may ask for more information or clarification. Reply quickly and accurately to keep the process moving.

These are the fundamental mortgage application steps for getting approved for a mortgage loan.

Key Factors Lenders Consider for Mortgage Approval

In considering your suitability to take a loan to purchase a house, three main areas will be considered by the lenders:

- Credit Score: A high credit score demonstrates that you responsibly utilise debt, and your likelihood of approval is high, and you may receive a lower interest rate.

- Income and Employment History: Lenders would want to have a steady income and good employment (at least 6-12 months in your current job, or more than 2 years of self-employment). They must be convinced that you are capable of repaying them regularly.

- Existing Debts and Expenses: Your Debt-to-Income (DTI) is important. This is a ratio of the amount you pay in terms of debt per month, in relation to your gross monthly income. A low DTI indicates that you have additional money to make a new mortgage payment.

- Deposit Size: The size of your deposit in relation to the value of the property (the Loan-to-Value Ratio or LVR) is important. The bigger the deposit (preferably 20% or over), the less risk the lender has, and you are likely to avoid Lenders Mortgage Insurance (LMI) loan in Melbourne.

- Property Type: There can be language that makes certain properties, such as extremely small apartments or properties located in high-risk locations, have more strict lending requirements or a higher deposit requirement.

These mortgage approval criteria are important to anyone intending to be approved for a mortgage loan.

Tips to Improve Your Chances of Getting Approved

When you are wondering how you can be approved for a mortgage loan, it is possible to increase your chances of being approved by trying the following tips:

- Reduce Existing Debts and Improve Credit Score: Since it is a priority, pay off credit card balances and personal loans. Ensure that all your bills are paid on time; this forms a big portion of your credit score.

- Save for a Larger Deposit: You have to target a 20% deposit to reduce your LVR and demonstrate your ability to save money.

- Avoid Large Purchases Before the Application: Do not make new loans, purchase a car or make big credit card purchases in the months before and during your application. Such activities boost your DTI and influence the amount of borrowing that you can do.

- Prepare All Documents Accurately: Inconsistencies or lack of any information a very frequent reasons to get delayed or rejected. Check everything two times before turning in.

- Consider a Mortgage Broker for Guidance: An expert Mortgage Broker can look into your application and recommend minor modifications to your financial situation, as well as forward your application to the lender that best fits your unique circumstances.

How Capkon Melbourne Helps You Secure Mortgage Approval

We take the stress out of getting approved for a mortgage loan. Capkon Melbourne offers:

- Expert Mortgage Brokers Who Assess Your Financial Situation: We guide you in realistically understanding your current strengths and standing in terms of finances and borrowing capacity, and will offer you specific advice to improve your submission.

- Guidance on Loan Products and Lenders Suited to Your Profile: Our experience with many lenders and understanding of which ones are best suited to your unique profile can save you time and help you avoid damaging your credit score through multiple applications.

- Assistance with Documentation, Applications, and Pre-Approval: We take care of paperwork and make sure that each and every form is duly filled out and all the required papers are submitted at the appropriate time.

- Ongoing Support Throughout the Mortgage Process: You have us to help you during your entire mortgage process, starting with the initial conversation with us to the settlement time. We are there to assist you in answering your questions and communicating with the lender.

Get the mortgage approval services you require with our team of Melbourne mortgage brokers! Contact us for a detailed consultation.

Common Mortgage Approval Mistakes to Avoid

Knowing what not to do is just as important as knowing how to get approved for a mortgage loan:

- Missing Documents or Inaccurate Information: Any inconsistency can raise a red flag for the lender and cause major delays or outright rejection.

- Overestimating Borrowing Capacity: Applying for more than you can comfortably afford can lead to rejection. Be realistic about your budget.

- Ignoring Credit Report Issues: Fix any errors or old negative listings on your credit report before you apply.

- Changing Jobs or Financial Situation During Application: Lenders want stability. Making major changes can put the approval process on hold.

Frequently Asked Questions (FAQ)

Q1: What is the difference between pre-approval and full mortgage approval?

A: Pre-approval is a conditional estimate of what you can borrow based on your personal finances. Full approval is the lender’s final promise to give you the loan after they have assessed the specific property you intend to buy.

Q2: How long does it take to get approved for a mortgage loan?

A: Pre-approval can take from a few days to two weeks. Full approval varies based on the lender and how complex your situation is, but usually takes 2-6 weeks from the time you submit your complete application.

Q3: Can I get approved with a low credit score?

A: It’s harder. While some specialist lenders may consider it, you will likely face stricter rules, a higher deposit requirement, and a higher interest rate. It’s best to improve your score first.

Q4: How much deposit do I need to increase approval chances?

A: A 20% deposit is best because it usually avoids Lenders Mortgage Insurance (LMI) and shows the lender you are low risk. You can apply with less (sometimes as low as 5%), but LMI will apply.

Q5: Does Capkon Melbourne help first-time buyers get approved?

A: Yes, we specialise in guiding first-time buyers through every step, helping them access government grants and schemes, and making the whole process simpler.

Q6: What documents are required for a mortgage application?

A: Typically, you’ll need recent payslips, tax returns, bank statements, proof of ID, and statements for all your existing debts (credit cards, loans).

Q7: Can I apply for multiple mortgage loans at once?

A: You can, but it is generally not recommended. Multiple applications mean multiple credit checks, which can slightly lower your credit score and signal to lenders that you are high-risk. Working with one broker who can compare multiple lenders for you is a smarter approach.

Do you need any Assistance in your loan?

We are here to help you.